Beyond the Mandate: Why a Choice of Credit Models Matters for SBA Lenders

Brett Caines

The required-model era is officially over. For SBA lenders, the primary question is no longer about clearing a mandatory regulatory bar. It is now about which credit model actually drives portfolio performance.

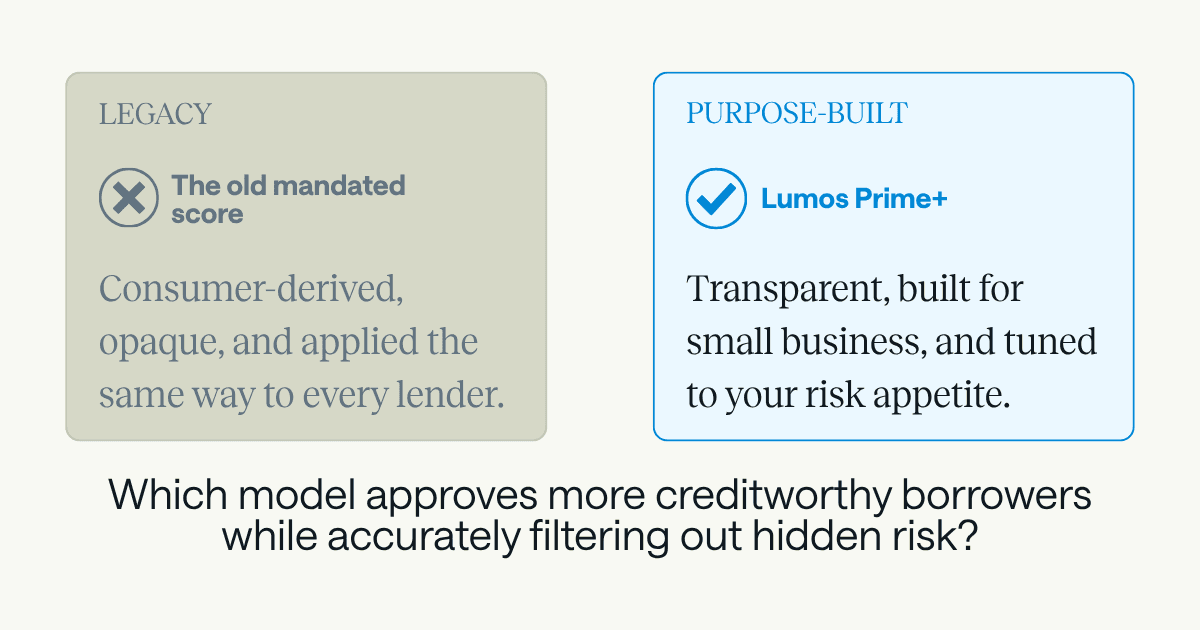

For nearly three decades, small business lenders utilizing the SBA 7(a) program didn’t choose their required credit scoring model. They were handed one. A single, opaque “black box” model sat at the front of the underwriting process, acting as an unavoidable prerequisite even if a lender was already paying to run their own internal scoring system.

In 2026, the landscape shifted. With the SBA officially sunsetting the mandatory use of a single, legacy scoring service for small 7(a) loans, institutions can finally rely exclusively on credit models optimized for their unique risk appetites, without a mandated score acting as a gatekeeper. It is a quiet regulatory rule change with a massive strategic implication: credit scoring is now a choice, not a mandate.

A Choice Is Only as Good as What You Do With It

Having options is only a competitive advantage if you actively use them. The path of least resistance is to stick with what is familiar and rely on legacy systems purely out of institutional habit. In a highly regulated environment, comfort often stifles innovation because change carries perceived risk.

However, forward-thinking lenders who embrace this new flexibility are asking a fundamental question they can finally act on without running redundant systems:

Which model approves more creditworthy borrowers while accurately filtering out hidden risk?

This is no longer a check-the-box compliance exercise. It is a direct test of portfolio performance, and performance is entirely measurable.

Evaluate on Evidence, Not Habit

When you have the autonomy to choose, your evaluation standard should be exceptionally clear. A high-performing credit model must achieve two distinct objectives simultaneously:

Surface strong borrowers that generic, consumer-derived models routinely overlook.

Isolate hidden risk within applications that legacy tools let slip through.

Succeeding at both allows you to safely expand your portfolio and protect your book without shifting your core risk appetite. It breaks the old industry assumption that growth and risk mitigation are mutually exclusive. You can have growth without increasing risk.

Furthermore, a scoring model must be purpose-built for the specific assets you are underwriting. Small business borrowers do not behave like typical consumers. Forcing a consumer-centric framework onto a commercial loan often leads to inaccurate assessments on borderline loan opportunities, which are the exact scenarios where precision matters most.

Lumos Prime+ was engineered exclusively for small business lending. It is trained on over 2 million small business loans and backed by 30 years of performance data spanning multiple economic cycles, ensuring resilience even during severe market downturns.

Crucially, it replaces the low-transparency guessing games of legacy systems with complete clarity. Prime+ provides high-transparency underwriting by returning the top 10 features driving the default risk for every single applicant. You are never left wondering what happened inside a black box, because you always know exactly why a score is what it is.

Prove It on Your Own Book

A newly unlocked operational freedom deserves more than a marketing brochure. It demands empirical proof on your own historical data.

Through our proof of concept, Lumos will retro-score your historical originations and declined applications. We will map our insights directly against your real-world outcomes to show you:

The missed opportunities: Creditworthy borrowers you may have turned away.

The hidden risks: High-risk approvals that could have been avoided.

The predictive edge: Whether Prime+ flagged past defaults before they impacted your balance sheet.

It is your book, your market, and your historical data. Let the predictive power of Prime+ prove itself with zero cost and zero friction to your current operations.

The Standard Is Yours to Set

Trusted by over 100 small business lending institutions and delivering decisions in seconds via the Lumos portal or direct LOS integration, Prime+ is built for the choice you can finally make.

The mandate is officially gone. The underwriting standard is yours to set.

Make your next move based on evidence. Schedule your portfolio retro-score today.

Book a 30-minute demo. No pressure, no sales pitch. Just a straightforward conversation about whether Lumos is right for you.

What To Expect:

Quick platform overview

Live demo with real loan examples

Discussion of your specific needs

Clear next steps

"The data and insights provided by Lumos have been instrumental in driving numerous policy changes within our organization."

VP, Senior Product Manager, US Bank

" height="29.26525980811059px" id="Eth71R0cp" transform="translate(50.52 7.877)" width="128.4356838868068px"/><path d="M 11.504 26.662 C 13.336 26.98 15.177 27.241 17.025 27.445 C 17.285 29.224 17.589 31.249 17.922 33.01 C 19.147 32.283 21.153 30.675 22.427 29.793 C 23.831 30.749 25.613 32.22 26.99 33.03 C 25.815 36.077 24.734 39.17 23.558 42.217 C 23.29 42.912 22.993 43.872 22.596 44.483 C 21.955 44.554 21.761 43.465 21.609 42.971 C 20.391 40.097 18.964 36.046 17.872 33.065 C 16.793 33.66 7.128 38.055 6.752 38.016 C 6.687 38.009 6.584 37.851 6.538 37.796 C 6.428 37.314 9.351 31.438 9.748 30.419 C 10.07 29.592 11.059 27.547 11.504 26.662 Z M 33.315 17.665 C 33.811 17.67 44.337 21.602 44.765 21.893 C 44.829 22.154 44.823 22.057 44.743 22.33 C 44.2 22.746 41.332 23.727 40.478 24.044 L 33.378 26.673 C 33.931 27.703 34.585 29.232 35.077 30.314 L 37.921 36.591 C 38.139 36.993 38.577 37.669 38.215 38.059 C 37.576 38.025 28.285 33.71 27.005 33.081 C 27.245 31.226 27.527 29.375 27.852 27.532 C 29.68 27.191 31.452 27.024 33.361 26.642 C 32.387 25.285 31.08 23.402 30.028 22.145 C 31.145 20.668 32.241 19.174 33.315 17.665 Z M 11.47 17.635 C 12.542 19.071 13.786 20.686 14.782 22.158 C 13.751 23.535 12.423 25.259 11.471 26.662 C 7.932 25.41 3.445 23.785 0 22.375 L 0 21.889 C 0.606 21.563 4.34 20.21 5.18 19.923 C 6.787 19.373 10.005 17.985 11.47 17.635 Z M 38.174 6.263 C 38.651 6.647 36.872 9.988 36.559 10.642 C 35.557 12.85 34.425 15.506 33.354 17.637 C 31.433 17.286 29.758 17.057 27.819 16.83 C 27.504 14.962 27.219 13.088 26.965 11.21 C 28.001 10.653 37.733 6.247 38.174 6.263 Z M 11.501 17.628 C 11.491 17.63 11.481 17.633 11.47 17.635 C 11.467 17.63 11.463 17.625 11.459 17.62 C 11.47 17.617 11.482 17.615 11.493 17.613 C 11.496 17.618 11.498 17.623 11.501 17.628 Z M 6.584 6.275 C 7.178 6.118 16.533 10.566 17.901 11.193 C 17.626 12.874 17.196 15.105 17.02 16.753 C 15.137 17.022 13.363 17.27 11.493 17.613 C 10.01 14.74 8.822 11.568 7.374 8.666 C 7.162 8.243 6.391 6.664 6.584 6.275 Z M 25.57 7.432 C 25.913 8.348 26.716 10.341 26.965 11.21 C 26.335 11.545 23.197 13.924 22.45 14.47 C 20.941 13.448 19.381 12.27 17.901 11.193 C 18.006 10.669 18.713 8.998 18.925 8.369 C 19.829 5.694 21.248 2.668 22.023 0 L 22.788 0 Z" fill="rgb(28, 26, 26)" height="44.486082377664px" id="u84SiQ2Nx" transform="translate(0 0.255)" width="44.80873390361835px"/></svg>)